Usual Response To Home Mortgage Questions

Article writer-Silva UlriksenBuying a new home can be fun if you do not get overly stressed during the approval process. There are many criteria you need to meet in order to finance your home and it is important to learn more about mortgages before you apply for one. You should keep reading for some useful tips on mortgages before making any important financial decisions.

When trying to figure out how much your mortgage payment will be each month, it is best that you get pre-approved for the loan. Look around so you know what your price range is. This will help you form a budget.

Consider unexpected expenses when you decide on the monthly mortgage payment that you can afford. It is not always a good idea to borrow the maximum that the lender will allow if your payment will stretch your budget to the limit and unexpected bills would leave you unable to make your payment.

Make sure you know how much you can afford before applying for a mortgage. Do not rely on what your lender says you can afford. Make a budget, allowing room for any unexpected expenses. Use online calculators which can help you estimate how much mortgage you can afford to pay monthly.

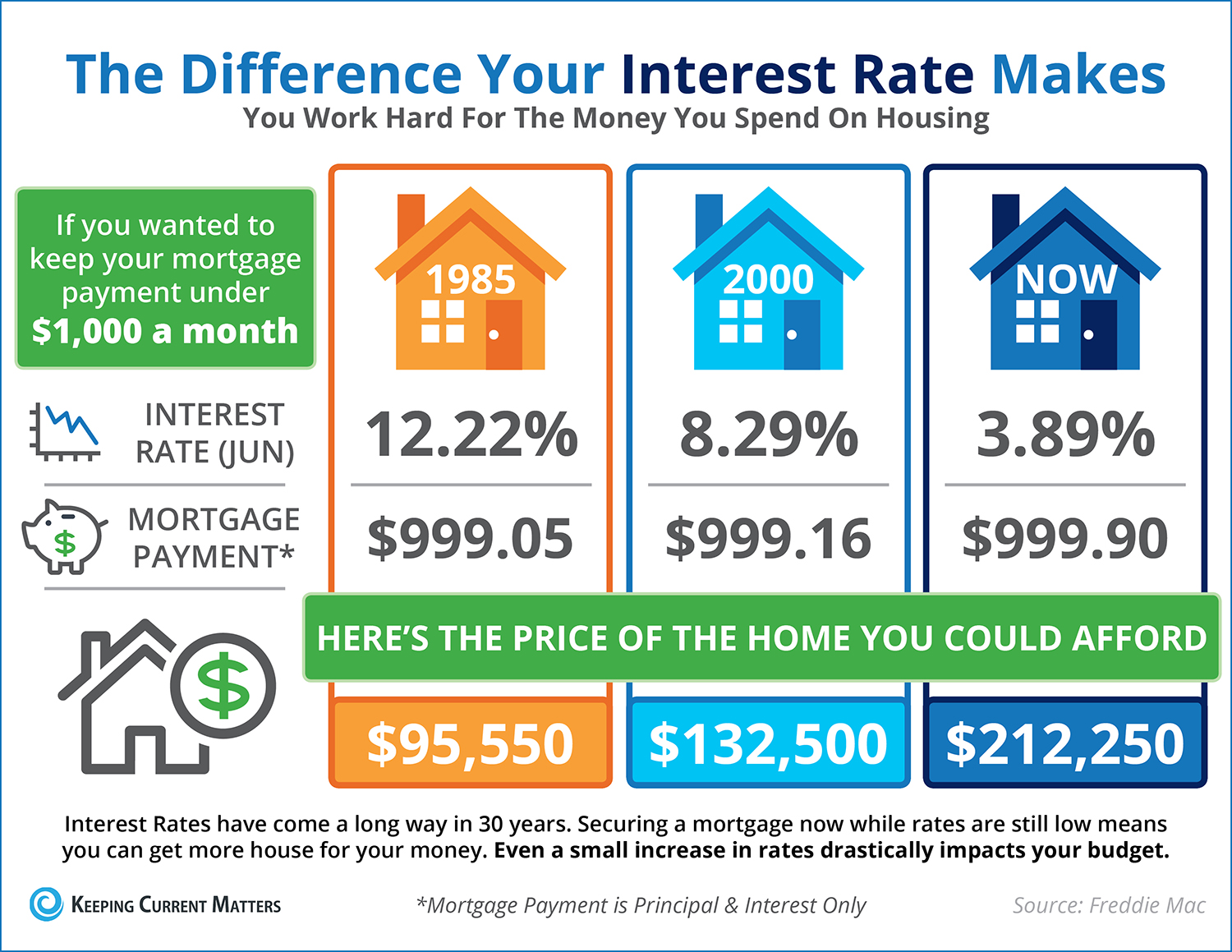

Your mortgage payment should not be more than thirty percent of what you make. Paying a lot because you make enough money can make problems occur later on if you were to have any financial problems. Manageable payments are good for your budget.

If your mortgage spans 30 years, think about chipping an additional monthly payment. This will help pay down principal. If you pay an additional amount on a routine basis, your can be paid off faster and your total interest liability can be a lot less.

Keep in mind that not all mortgage lending companies have the same rules for approving mortgages and don't be discouraged if you are turned down by the first one you try. Ask for an explanation of why you were denied the mortgage and fix the problem if you can. It may also be that you just need to find a different mortgage company.

Monitor interest rates before signing with a mortgage lender. If the interest rates have been dropping recently, it may be worth holding off with the mortgage loan for a few months to see if you get a better rate. Yes, it's a gamble, but it has the potential to save a lot of money over the life of the loan.

Remember that your mortgage typically can't cover your entire house payment. You need to put your own money up for the down payment in most situations. Check out your local laws regarding buying a home before you get a mortgage so you don't run afoul of regulations, leaving you homeless.

Use local lenders. If you are using a mortgage broker, it is common to get quotes from lenders who are out of state. Estimates given by brokers who are not local may not be aware of costs that local lenders know about because they are familiar with local laws. This can lead to incorrect estimates.

There are many different types of home mortgage loans available, and some are much easier to get than others. If you are having a problem getting a conventional loan, try applying for an adjustable rate mortgage or a balloon. These are short term loans ranging from one to 10 years, and need to be converted when they expire.

Be careful when taking out a second line of financing. Many financial institutions will allow you to borrow money on your home equity to pay off other debts. Remember you are not actually paying off those debts, but transferring them to your house. Check to make sure your new home loan is not at a higher interest rate than the original debts.

After getting a home loan, try paying a little extra on the principal each month. This will help you pay off your loan much faster. For instance, if you pay a hundred dollars more toward your principal, you can reduce your loan term by ten years or more.

Don't take out a mortgage for the maximum amount the bank will lend you. This was a strategy that backfired on thousands of people a few short years ago. They assumed housing values would inevitably rise and that payment would seem small in comparison. Make out a budget, and leave yourself plenty of breathing room for unexpected expenses.

Consider a shorter term of 20 or 15 years for your mortgage if you are able to handle a higher monthly payment. Shorter-term mortgages come with lower interest rates, though they also require higher payments each month. Overall, you will save thousands this way.

Never assume that a good faith estimate is fact or written in stone. It is in fact not just an estimate, but one written in good faith. Always be wary of extra costs and fees that can creep into the official and formal paperwork later that drive up your total expense.

Be sure that you know exactly how long your home mortgage contract will require you to wait before it allows you to refinance. Some contracts will let you within on year, while others may not allow it before five years pass. What you can tolerate depends on many factors, so be sure to keep this tip in mind.

Save some money before applying for a mortgage. Required down https://economictimes.indiatimes.com/industry/banking/finance/arya-ag-ties-up-with-mas-financial-services-to-offer-agri-finance-to-farmers/articleshow/89428829.cms vary, but you probably want to have no less than 3.5% available. The higher it is, the better it may be for you. If you take a private mortgage, you'll need to pay extra if you put less than 20 percent down.

Before you buy a home, you need a home mortgage. You have to have a bit of education before you start the process of applying, though. Use https://www.forbes.com/sites/davidbirch/2021/09/16/digital-identity-should-be-a-big-business-for-banks/ to get the loan you want.